Filing Process for DUI-Related Insurance Explained

Steering through the filing process for DUI-related insurance can feel overwhelming, but understanding the steps is essential. After a DUI conviction, you'll need to secure an SR22 form from your insurance provider, which confirms your compliance with state minimum insurance requirements. This form isn't just a piece of paper; it's important for maintaining your driving privileges. What happens if you let your coverage lapse? The consequences could be significant, prompting further exploration of this complex topic.

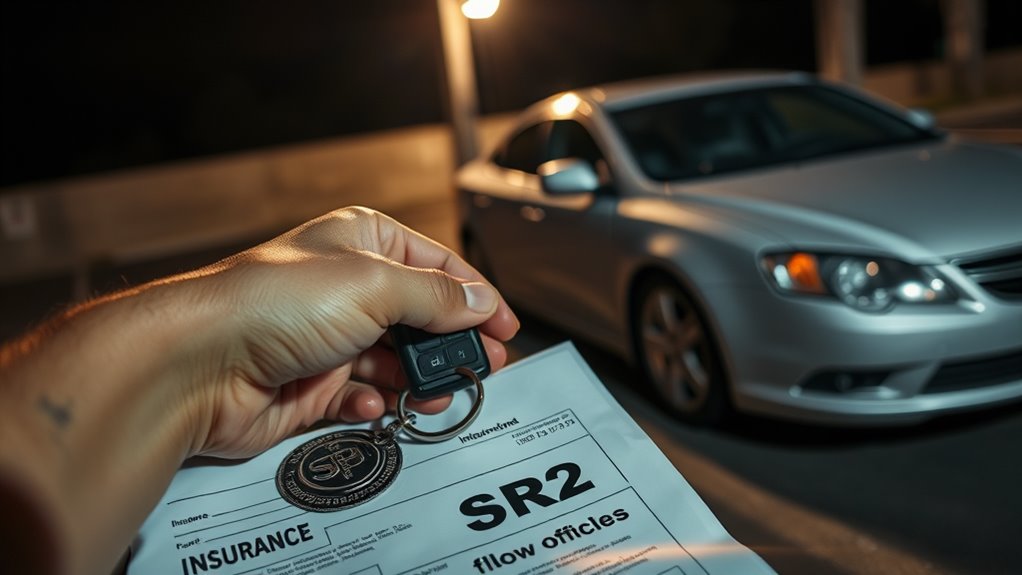

Have you recently faced a DUI charge and are unsure about the insurance filing process? Understanding the steps involved in filing for an SR22 can help you navigate this challenging time. After a DUI conviction, many states require you to file an SR22 form, which serves as a certificate of financial responsibility. This document proves you have the minimum required insurance coverage. Your insurer typically charges a small fee, ranging from $15 to $25, for the SR22 filing. The specifics of the filing process can vary considerably from state to state, so it's essential to familiarize yourself with your local requirements.

Once your insurer files the SR22 with the state, they'll notify the relevant authorities about your compliance. This notification is important for reinstating your driver's license, which is often suspended due to a DUI conviction. In many cases, you can't regain your driving privileges without the SR22. Additionally, some states may require the installation of ignition interlocks alongside the SR22 as part of the license reinstatement conditions. These measures are typically mandated by the court and are designed to guarantee that you can safely operate a vehicle.

It's worth noting that a DUI conviction can lead to a substantial increase in your insurance rates. On average, drivers with a DUI face an 80% hike in their insurance costs. However, this increase can vary widely depending on your state. Insurers categorize DUI offenders as high-risk drivers, which drives up premium rates. To mitigate these costs, you can compare quotes from different insurers. This process can help you identify more affordable options tailored to your specific circumstances. Consider exploring affordable SR-22 insurance options to further reduce your financial burden during this time.

You might also consider a non-owner SR22 policy if you don't own a vehicle but still need to demonstrate financial responsibility. This type of coverage is important for those who frequently drive others' vehicles. Non-owner policies fulfill the same requirements as standard SR22 filings, guaranteeing you maintain compliance with the law. Some states may also require a driver safety course to help ensure that you are capable of safe driving practices. Shopping around for the best rates in this category is also advisable, as different insurers may offer varying terms.

Maintaining compliance is essential after you file an SR22. Your insurance provider is responsible for monitoring your coverage status and reporting any lapses. If there's a lapse in your policy, it could lead to an immediate suspension of your driving privileges. Insurers regularly check driving records to verify you meet the SR22 requirements, so staying on top of your policy is crucial.

Conclusion

Maneuvering the filing process for DUI-related insurance, particularly with an SR22, may seem intimidating, but it's essential for regaining your driving privileges. You might worry about the costs or increased premiums, but maintaining your SR22 can ultimately lead to lower rates over time as you rebuild your driving record. Staying compliant not only protects your license but also demonstrates responsibility, which can help you secure better insurance options in the future. Take the first step today.